Ready to apply for a credit card but worried that your three-digit credit score is just too low?

Don’t. It’s true that you’ll need a better credit score to qualify for cards that accompany generous rewards programs and low interest rates, but although your score is a smaller amount than stellar, you’ll still qualify for a credit card .

Juan Carlos Cruz, founding father of Britewater Financial Group in Brooklyn, New York, explained that the connection between credit cards and credit scores isn’t a mysterious one.

“The higher your credit score, the more favorable credit cards you’ll receive,” Cruz said. “If you’ve got missed payments otherwise you are using most of the credit available to you already, those are signs that you simply aren’t using your trade lines responsibly. You won’t qualify for the higher cards due to that.”

Here’s a glance at the credit scores you’ll got to qualify for everything from no-frills basic credit cards to those offering big sign-up bonuses and hefty cash back bonuses.

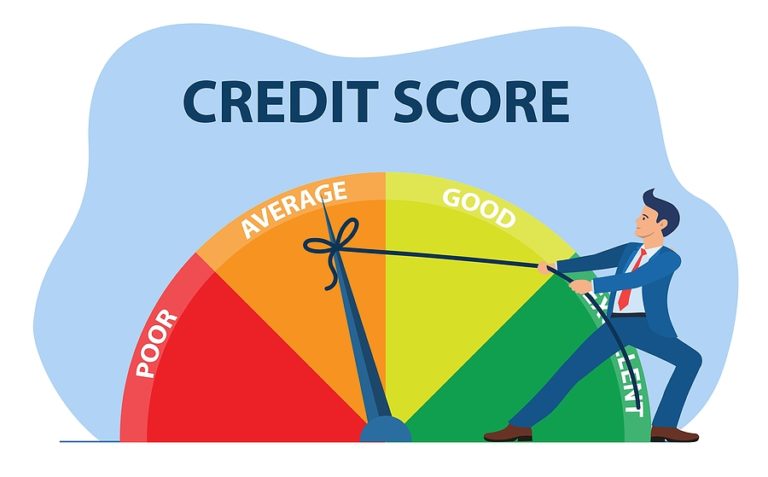

What is a credit score?

Your credit score provides a fast check out how well you’ve paid your bills and managed your credit. the less dings – like late payments, missed payments or high credit card balances – in your credit history, the upper your score are going to be .

FICO credit scores are the foremost important sort of credit score when you’re applying for credit or loans because they’re those lenders and banks typically consider when judging borrowers. These scores run from a coffee of 300 to a high of 850. Most lenders consider FICO many 740 or higher to be excellent, and, if your score is that prime , you ought to have little problem qualifying for the simplest credit cards.

Your score is formed from the knowledge found on your three credit reports, one each maintained by the national credit bureaus of Experian, Equifax and TransUnion. These reports include several items:

- Balances on your credit cards and loans

- Any payments made 30 days or more after your maturity on your credit card or loan accounts during the last seven years

- Any bankruptcy filings within the last seven or 10 years

- Any foreclosures on your record during the last seven years

While you’ll access each of your credit reports for free of charge once a year at AnnualCreditReport.com, you can’t get your official FICO score for free of charge . you’ll pip out , though, from myFICO.

You can also get free credit scores, although these often aren’t an equivalent FICO scores that lenders or credit card companies see once you apply. you’ll usually get these credit scores from your credit card companies, bank or depository financial institution . And although these aren’t “official” FICO scores, they’re going to offer you an honest idea of how strong your credit is.

What credit score is required for a credit card?

Tom Giancola, chief credit risk officer with Mercury Financial, which has offices in Austin, Texas, and Wilmington, Delaware, said that buyers typically need a FICO score within the low 600s to qualify for a basic, no-frills mastercard . For a basic rewards card, you’d need a score within the mid 600s to the low 700s.

And to qualify for premium cards with the foremost valuable rewards programs? that sometimes requires a FICO score of 740 or higher, consistent with Giancola.

“Those rewards are expensive,” Giancola said. “The banks can’t tolerate high loss levels if they’re paying out that much in rewards expense. in order that they reserve these cards for the safest of applicants.”

Click here to check out Credit Calculators.

How to improve your score for better cards

If you would like to enhance your credit score, take two main steps. First, pay your credit card bills and any loans, like student loans or a mortgage, on time monthly .

Next, if you’ve got credit card debt, pay off the maximum amount as you’ll . Using less of your credit limits will boost your score. Just make certain to not close any credit cards that you simply pay off, since closing the accounts will offer you less available credit and hurt your credit score by lowering your credit utilization ratio.

Andrea Woroch, a consumer-savings expert in Bakersfield, California, said that another key to improving your credit score is to eliminate the negative spending habits that contribute to credit card debt. “Identifying and eliminating triggers that cause impulse buys is vital to keeping your credit in tip-top shape,” Woroch said.

Woroch recommends that those that struggle with impulse buying should delete deal apps from their phones and unsubscribe from store newsletters to assist eliminate the temptation to overspend.

What credit card am I able to get with bad credit?

Credit bureau Experian defines a really poor FICO score as being within the 300 to 579 range. If your score falls during this range of bad credit, you’ll most frequently qualify for secured credit cards. These operate a bit like traditional credit cards, except their credit limits are tied to a deposit you create when applying for the cardboard . for instance , you would possibly deposit $500 with the cardboard issuer then receive a secured credit card with a maximum credit limit of $500.

It’s easier to qualify for these cards because banks are protected. If you fail to form your payments, the bank pays them off using your deposit.

A good option is that the Chime Credit Builder Visa card. This card charges no annual fee and requires no margin . It also charges no interest. this is often still a secured credit card, but it had been created to be paired with the Chime Spending Account. To use this card, you initially open a spending account then transfer money from that account to your Credit Builder credit card. that cash you’ve transferred over acts as your credit limit.

You can qualify for other credit cards albeit your credit is bad, including the Indigo® Platinum Mastercard® or the Secured Mastercard® from Capital One. Just remember that such cards usually accompany annual fees.

Few secured credit cards offer rewards, with the Discover It® Secured credit card being an exception. you’ll earn 2% cash back at gas stations and restaurants (up to $1,000 in purchase per quarter) and 1% back on all other purchases. This card doesn’t charge an annual fee, but you’ll got to make a margin .

What credit card am I able to get with fair credit?

Experian defines a good FICO credit score as starting from 580 to 669. If your credit score is within the fair range, you’ll qualify for a greater number of credit cards, including people who don’t charge annual fees or require security deposits.

The Capital One Platinum credit card may be a good option if your credit score falls within the lower end of the fair range. this is often a basic card that doesn’t offer any rewards. However, it also doesn’t charge an annual fee, meaning you’ll easily use this card to assist build your credit.

An option if your score is on the upper end of the fair range is that the Credit One Bank® Visa® for Rebuilding Credit. This card offers a rewards program, supplying you with 1% back on purchases for gas, groceries and phone services. However, you’ll pay an annual fee of $0–$95 the primary year and $0–$99 annually after.

What credit card am I able to get with good or excellent credit?

If your FICO score is above 670, it’s within the good credit category. And if it’s 740 to 799 it falls into the excellent slot. Finally, Experian says that any score of 800 or more is taken into account exceptional. With scores like these, you’ll qualify for nearly any credit card on the market.

The Blue Cash Preferred® Card from American Express may be a exemplar . This card provides 6% cash back at U.S. supermarkets (up to $6,000 per annum in purchases, then 1%) and on select U.S. streaming services. You’ll also get 3% back at U.S. gas stations and for taxis, rideshare services, parking, trains, tolls and buses. You’ll receive 1% cash back on all other purchases. You’ll also earn a $300 statement credit if you charge a minimum of $3,000 within the primary six months of opening your card.

The Discover it® Cash Back is another strong card. With this card, you’ll receive 5% cash back on bonus categories that rotate each quarter after you activate (on up to $1,500 in combined quarterly spending, then it’s 1%), also as 1% cash back on general purchases.

How to get a credit card with no credit

Some people don’t have good or bad credit because they simply don’t have enough credit history to possess any credit score in the least . It are often difficult for people that don’t have loans or credit cards to create a credit history. and people with no credit scores might struggle to qualify for many credit cards.

A good option for those with no credit history may be a secured credit card. Similarly to if you’ve got a poor credit score, banks are more likely to approve you for a secured card because there’s less risk to the bank because of that margin you set down.

“The bank already has your money,” said Cruz. “There’s no reason, then, for them to feel in danger . they’re going to not be hurt financially if you don’t pay.”

Once you get that secured card, use it monthly . As you pay off your bill fully with on-time payments monthly , you’ll slowly build a solid credit score.

Giancola recommends that buyers who got to build a credit history consider private-label cards, too. These are credit cards issued by department shops , wholesale clubs and other retailers which will only be used at one specific store, and that they rarely accompany generous perks.

But Giancola says that it’s easier to qualify for these cards because they aren’t as risky as traditional credit cards. And if consumers use them properly – charging what they will afford to pay off fully monthly and paying their bills on time – they will build up a solid credit history to qualify for more traditional credit cards down the road.

For those with no credit score, Giancola also recommends signing up as a licensed user on someone else’s credit card account to assist build a credit history. once you do that , you’re added as a user on someone else’s credit card account. The account’s primary cardholder is liable for paying the bill monthly , but the payment is reported to the credit bureaus in both that person’s name and your name, which helps you build a positive credit history. Just take care to only use the cardboard as prescribed with the first cardholder so you don’t ruin your relationship thereupon person.

Bottom line

Whether it’s a secured card or a top-tier rewards or travel card, you’ll find the proper card for your credit score. If you’re starting with a coffee (or no) credit score, you’ll build your credit history through responsible use to eventually qualify for the credit cards you would like .

Source: What credit score do you need for a credit card?

For more blog, please visit: https://creditcalculators.org/